Facebook

Facebook

Twitter

Twitter

Pinterest

Pinterest

Copy Link

Copy Link

Is The Window Closing?

|

|

With interest rates lower than they’ve been in over 40 years, it may be difficult to think of a “window of opportunity” closing. However, it isn’t difficult to understand that it may very probably cost more to live in a home in the near future due to rising interest rates and prices.

Zillow recently reported results from a nationwide study that home values are expected to appreciate by 4.5% through the end of the year. Coupled with Freddie Mac’s projection that rates are going up, the cost of housing for buyers by the end of the year will be higher than it is now.

While uncertainty of the future can stagnate some people, the fear of loss can be much more devastating when a person realizes that the amount they pay to live and enjoy a home could have been considerably lower had they acted when prices and mortgage rates were lower.

The following example considers a $250,000 purchase today with a FHA mortgage compared to what it might be at the end of the year with a higher price and interest rate as discussed earlier. The net effect is that it will cost $191.87 to live in the very same home based on the cost of waiting to buy.

To see what the cost might be for your price range, use this Cost of Waiting to Buy spreadsheet.

|

|

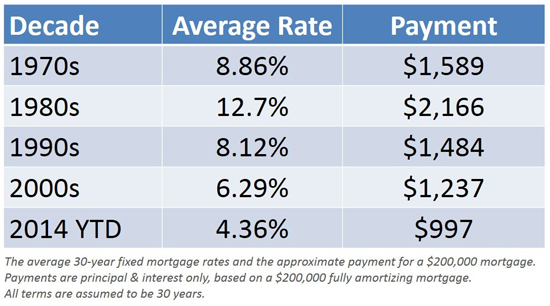

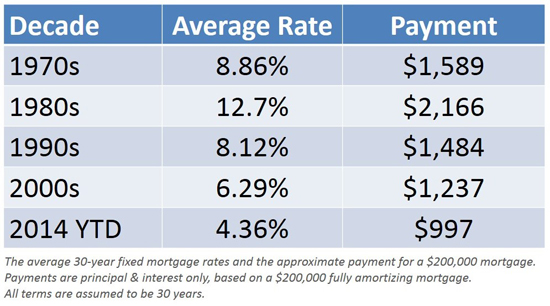

Interest Rates Are Not Getting Any Lower!

"One thing seems certain: we aren't likely to see average 30-year fixed mortgage rates return to the historic lows experienced in 2012."

– Freddie Mac, March 24, 2014

There are those that hope that 30-year mortgage interest rates will head back under 4%. Obviously, for any prospective home purchaser that would be great news. However, there is probably a greater chance that interest rates will return to the greater than 6% rate of the last decade before they would return to theless than 3.5% rate of 2012.

Freddie Mac, in one of four original posts on their new blog, explained that current rates are still extremely low compared to historic averages:

"The all-time record low – since Freddie Mac began tracking mortgage rates in 1971 – was 3.31% in November 2012. Conversely, the all-time record high occurred in October of 1981, hitting 18.63%. That's more than four times higher than today's average 30-year fixed rate of 4.32% as of March 20…rates hovering around 4.5% may be high relative to last year, but something to celebrate compared to almost any year since 1971."

If you are thinking of buying a home, waiting for a dramatic decrease in mortgage rates might not make sense.

Looking For The Largest Deduction?

|

|

IRS allows taxpayers the option to take the standard deduction or the itemized deduction. The astute taxpayer will compare to see which one will result in the greatest deduction and the election can be made each year.

The 2013 standard deduction for a married couple filing jointly is $12,200 and $6,100 for a single taxpayer. It doesn’t require any proof of actual expense and has no requirement for home ownership.

Items that can be included on Schedule A for itemized deductions include:

- Certain taxes paid for state and local income tax, general sales tax, real estate property taxes, personal property taxes or other taxes paid

- Qualified home mortgage interest, investment interest or possibly, mortgage insurance premiums

- Charitable contributions

- Casualty or theft losses

- Medical and dental expenses that exceed 7.5% of adjusted gross income if born before 1/2/49 or 10% if born after 1/2/49

- Job expenses and other miscellaneous deductions that exceed 2% of adjusted gross income

A non-homeowner taxpayer who has been taking the standard deduction needs to consider that it isn’t just the ability to deduct the mortgage interest and property taxes.

While the standard deduction might be the obvious choice for a non-homeowner, the combination of the mortgage interest and the property taxes plus other allowable deductions not recognized previously such as charitable contributions, now makes taking the itemized deductions significantly more advantageous.

5 Things To Know About VA Loans

We are pleased to welcome Phil Georgiades as our guest blogger today. Phil is the Chief Loan Steward for VA Home Loan Centers, a veteran and active duty military services organization. – The KCM Crew

VA loans are the most misunderstood mortgage program in America. Industry professionals and consumers often receive incorrect data when they inquire about them. In fact, misconceptions about the government guaranteed home loan program are so prevalent that a recent VA survey found that approximately half of all military veterans do not understand it.

VA loans are the most misunderstood mortgage program in America. Industry professionals and consumers often receive incorrect data when they inquire about them. In fact, misconceptions about the government guaranteed home loan program are so prevalent that a recent VA survey found that approximately half of all military veterans do not understand it.

With this in mind, we would like to debunk the most common myths about VA Loans.

Myth 1: The VA loan benefit has a “one time” use.

Fact: Veterans and active duty military can use the VA loan many times. There is a limit to the borrower’s entitlement. The entitlement is the amount of loan the VA will guarantee. If the borrower exceeds their entitlement, they may have to make a down payment. Never the less, there are no limitations on how many times a Veteran or Active Duty Service Member can get a VA loan.

Myth 2: VA home loan benefits expire if they are not used.

Fact: For eligible participants, VA mortgage benefits never expire. This myth stems from confusion over the veteran benefit for education. Typically, the Montgomery GI Bill benefits expire 10 years after discharge.

Myth 3: A borrower can only have one VA loan at a time.

Fact: You can have two (or more) VA loans out at the same time as long as you have not exceeded your maximum entitlement and eligibility. In order to have more than one VA loan, the borrower must be able to afford both payments and sufficient entitlement is required. If the borrower exceeds their entitlement, they may be required to make a down payment.

Myth 4: If you have a VA loan, you cannot lease the home.

Fact: By law, homeowners with VA loans may rent out their home. If the home is located in a non-rental subdivision, the VA will not guarantee the loan. If the home is located in a subdivision (such as a co-op) where the other owners can deny or approve a tenant, the VA will not approve the financing. When an individual applies for a VA loan, they certify that they intend on making the home their primary residence. Borrowers cannot use their VA benefits to buy property for rental purposes except if they are using their benefits to buy a duplex, triplex or fourplex. Under these circumstances, the borrower must certify that they will occupy one of the units.

Myth 5: If a borrower has a short sale or foreclosure on a VA loan, they cannot have another VA loan.

Fact: If a borrower has a claim on their entitlement, they will still be able to get another VA loan, but the maximum amount they would otherwise qualify for may be less. For example, Mr. Smith had a home with a $100,000 VA loan that foreclosed in 2012. If Mr. Smith buys a home in a low cost area, he will have enough remaining eligibility for a $317,000 purchase with $0 money down. If he did not have the foreclosure, he would have been able to obtain another VA loan up to $417,000 with no money down payment.

Veterans and Active duty military deserve affordable home ownership. In recent years, the VA loan made up roughly 13% of all home purchase financing. This program remains underused largely because of misinformation. By separating facts from myth, more of America’s military would be able to realize their own American Dream.